“The pace of population growth in 2021 was five times slower in 2021 than over the preceding decade,” says Pew’s Joanna Biernacka-Lievestro, an author of the report and associate manager of Fiscal 50. “That’s notable because growth in the 2010s was already the slowest it had been since the Great Depression.”

Unlike its total size, the growth rate of the U.S. population has declined continuously since the first census in 1790. The rate went down steeply between 1880 and 1930, with an uptick in the years following the Great Depression.

Growth may be slowing, but the country’s total population is projected to grow 14 percent by 2050, bolstered by immigration. In 2021, gains from international migration were greater than gains from natural increase. (According to a 2021 Gallup poll, 42 million people in Latin America and the Caribbean alone would move to the U.S. if they could.)

The median cumulative annual growth rate between 2010 and 2020 was 0.55 percent, but 12 states achieved almost twice this, or more. No matter which direction growth rate or total population goes in a state, economic balance is affected.

Winners and Losers

“Over the years, we’ve seen that people have been moving from the Northeast and Midwest towards the West and South,” says Biernacka-Lievestro. “People are looking for a cheaper cost of living, or nicer weather.”

California is an outlier in this regard; it saw a population decline of almost 0.7 percent in 2021. Aside from the state’s high cost of living, an analysis from Stanford’s Hoover Institution found that the rate at which business headquarters left the state doubled in 2021.

The authors attribute this to factors including tax and regulatory policies; the labor, litigation and energy costs in the state; and “concerns about a declining quality of life.” Even so, the Golden State remains the world’s fifth-largest economy.

Some of the shifts seen in 2021 could be the consequence of remote work decisions that may be rethought if workers become confident that the bridge away from pandemic restrictions has truly been crossed, or if employers decide to reign in free-range employees. It’s too early know how this might unfold.

Texas added the most new residents, but Idaho and Utah had higher growth rates. Thirty-eight states grew more slowly in the 2010s than the 2000s, including California and Florida. Population losses were greatest in New York, Illinois, Hawaii and California, which the Pew researchers attribute to residents moving out of state.

Three of the states that lost population in the last year — West Virginia, Mississippi and Illinois — have been shrinking over the past decade. On the other hand, Vermont, Connecticut, Maine and New Hampshire grew at a faster rate than in the previous decade.

Population and Economy

“When you look at the long term, the past 10 years, states that had strong population growth also had strong economic growth,” says Biernaca-Lievestor. “States that were at the bottom in population growth were at the bottom of economic growth in terms of personal income.”

Workers are a fundamental building block for state economies, and population losses raise fears that tax revenue shortfalls will make it difficult for states to sustain commitments such as public-sector employee pensions, or provide services at the level residents need or expect.

Even without shifts due to relocation, demographic trends such as reduced birth rates, millions of women leaving the workforce and an over-65 population growing faster than the generations who will replace them, make it harder than ever to balance needs and resources.

Incentives for relocation are becoming more common. The Vermont New Relocating Worker grant program offers up to $7,500 in reimbursement to new residents who come to the state to fill jobs from employers in occupations qualified under the program. West Virginia is offering $12,000 to remote workers who come to the state. Move to Michigan offers up to $15,000 toward the purchase of a home in Southwest Michigan.

Even states that have seen gains face long-term challenges rallying larger and larger numbers of workers. That doesn’t necessarily mean their economies are rolling inevitably toward a dead end.

More Than a Numbers Game

Joel E. Cohen, a professor of populations at Rockefeller University and Columbia University in New York City, believes the notion that economic strength is based entirely on numbers is obsolete by centuries. He’s not convinced that slowed growth rates or population shifts mean the U.S. is headed for “demographic doom.”

“There is a mentality that says the bigger the level of economic activity, the better, and that to me is erroneous,” says Cohen. “What counts is not only economic activity, but economic activity per person.”

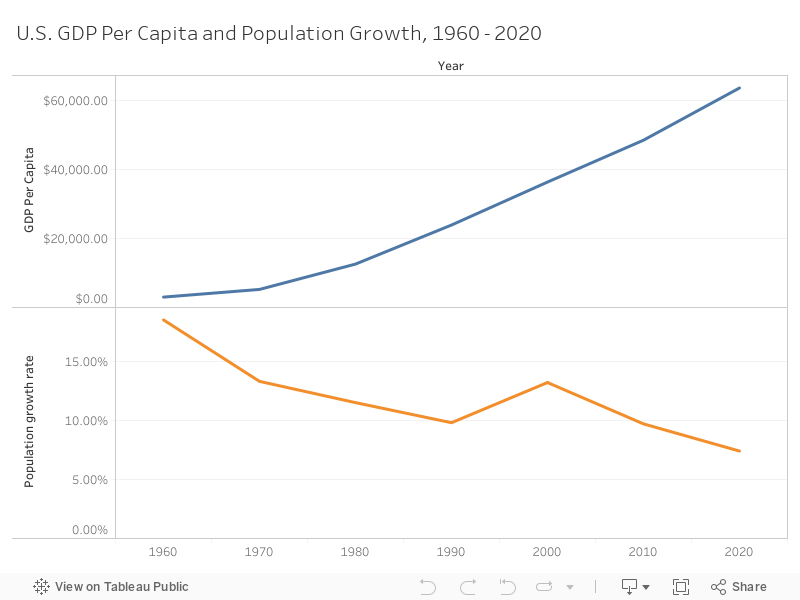

Two trends make it clear that population growth and productivity are not inextricably connected in the modern age. Between 1960 and 2020, the population growth rate decreased 60 percent, from 18.5 percent to 7.4 percent. Over this same time period, GDP per capita increased twentyfold. Between 2000 and 2020, GDP more than doubled, while the population growth rate dropped from 13.2 to 7.4 percent.

Workforce participation rates are the lowest they have been in 10 years. Advancing technology is eliminating an increasing number of the low-paying jobs that workers have fled during the Great Resignation. But many workers who have left the workforce don’t have the skills they need to access the better-paying jobs they want, or the skills employers in a technology-driven economy need to grow their companies.

Investments in the unskilled, underserved and underemployed could more than offset the impact of a reduced local workforce. Skilled workers are essential to the energy and infrastructure markets and to the long-term viability and resilience of communities. Billions in federal funding are available to jump-start training and careers.

“It’s not that the United States is on the verge of going out of business,” says Cohen. “We’re not making efficient use of the people we’ve got — why don’t we invest in them?”

Balancing the Equation

Cohen, who holds doctoral degrees in both applied mathematics and public health, has a broad view of the factors that comprise a healthy economy, including a need to invest now in public health to protect against economic disruption from a future pandemic. “Believe me, there will be one,” he says.

Population contraction might create short-term difficulties in meeting the needs of pensioners or others who depend on public funds, but if meeting such obligations depends on growth alone, he says, demographic expansion would have to continue indefinitely. This bumps up against the fact that growth and economic activity are constrained by the availability of natural resources.

Earth is already more populated than it has ever been, and it’s not going to get bigger. Slower population growth can mitigate human impacts on the environment, from warming, deforestation, loss of biodiversity and pollution to demand for finite water and land capacity.

Moreover, not everything that contributes to economic growth leads to the well-being of citizens. The bigger the private prison industry in a state, the bigger its contribution to GDP. “Is it better for people to have a larger prison population?” says Cohen. “I don’t think so.”

“The point of the economy is to make people well off, not the reverse. It’s not the point of people to make the economy grow.”

Digital Editor Zoe Manzanetti contributed to this article.

Related Articles